Disclaimer: The author of the content below is not a medical professional and does not have any medical training. As such, the contents on this page, including text, graphics, images, and any other material are for informational purposes only. The Content is not intended to be a substitute for professional medical advice, diagnosis, or treatment. Our full medical disclaimer can be found by clicking here.

I’ve tried to shy away from putting the medications that James is taking on here. The purpose of this blog is not to promote certain medications, or to say “hey, try this drug, it worked amazing for James.” I am not a doctor, nor do I have any sort of medical training, so I don’t have the knowledge to discuss prescription medications. This is a subject best discussed with your doctor or a medical professional. Besides, what works for James, may or may not work for you or your child.

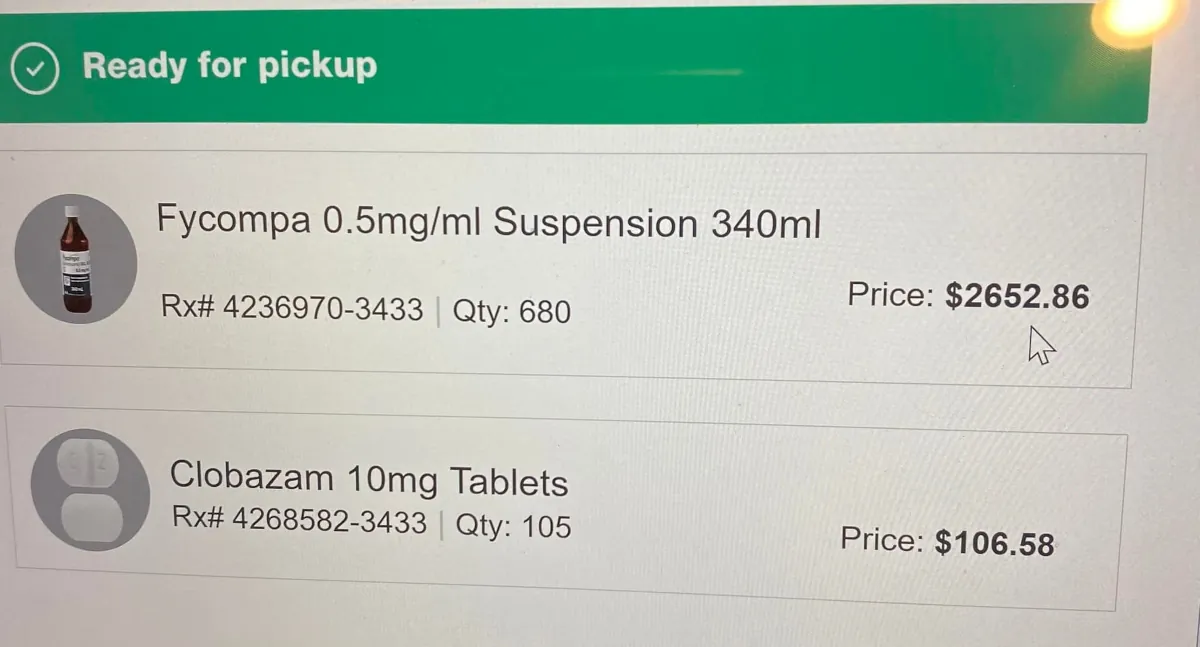

I am making an exception here to make a point. This is a screen shot of an email that Stacy received for two of James’ meds that were ready to be picked up, and what they are going to cost.

Like I said, I am not a medical professional, and I know nothing about the pharmaceutical industry. I am sure that a lot of research, development, testing and what-not goes into making medications. I also know that pharmaceutical companies, like all other companies, are in business to make money. But just how much money are they making, and why is there such a difference between per unit prices between various drugs? Using the above medications as an example, $2,652.86 divided by 680 equals approximately $3.90 per unit. For the other medication, it’s $106.58 divided by 105, which equals $1.01 per unit. What makes the first medication 3.86 times more than the second one?

I should mention that the prices above are after our primary insurance, so those prices are what we’re supposed to pay out of pocket for just two of James’ meds. I should also mention that it is the beginning of the year, and our deductible has not been met yet. Once we meet our deductible, our insurance will cover a lot more of that cost. So, what are we supposed to do until then? Fortunately, we can pull that money out of James’ medical fund. That’s what it’s there for. And fortunately, James has secondary insurance through the state that should cover the cost that our primary insurance doesn’t cover. But what about families that don’t have those two options? Are they supposed to choose between paying for their medications and paying for their rent, mortgage, car payment, utilities, or food?

Stacy posted the above picture on her Facebook page and looking at some of the comments, I know we’re not alone.

“Jayden’s is that price for 105mls for 13 days of medicine!”

“Fycompa is expensive but it works for Finnian. Our co-pay is $1742.91 a month but thankfully his other insurance pays the co-pay. It will be another few years before a generic will be allowed and even then it will be expensive”

“My oldest son always reads the “insurance saved you” section of our pharmacy printouts when we pick them up. The kids are blown away by how much their meds cost. We have 54 prescriptions currently. Without dual insurance we would be bankrupt.”

“My Xarelto is billed to my insurance $1300 for a 90 day script. My insurance charged me $100. I activated a discount card through the manufacturer, and I pay $10.”

“Garretts one medicine is 900 without insurance is crazy”

Yes, it is crazy. I am grateful for the drugs that available to James, but at the same time I am appalled by the prices that some of them cost. Something has to be done. Or at least show us justification for the high prices.

{kind=link}